AS THE FED RAISES RATES, JANET YELLEN’S LEGACY IS PONDERED

Donald Trump has the chance to mould America’s central bank

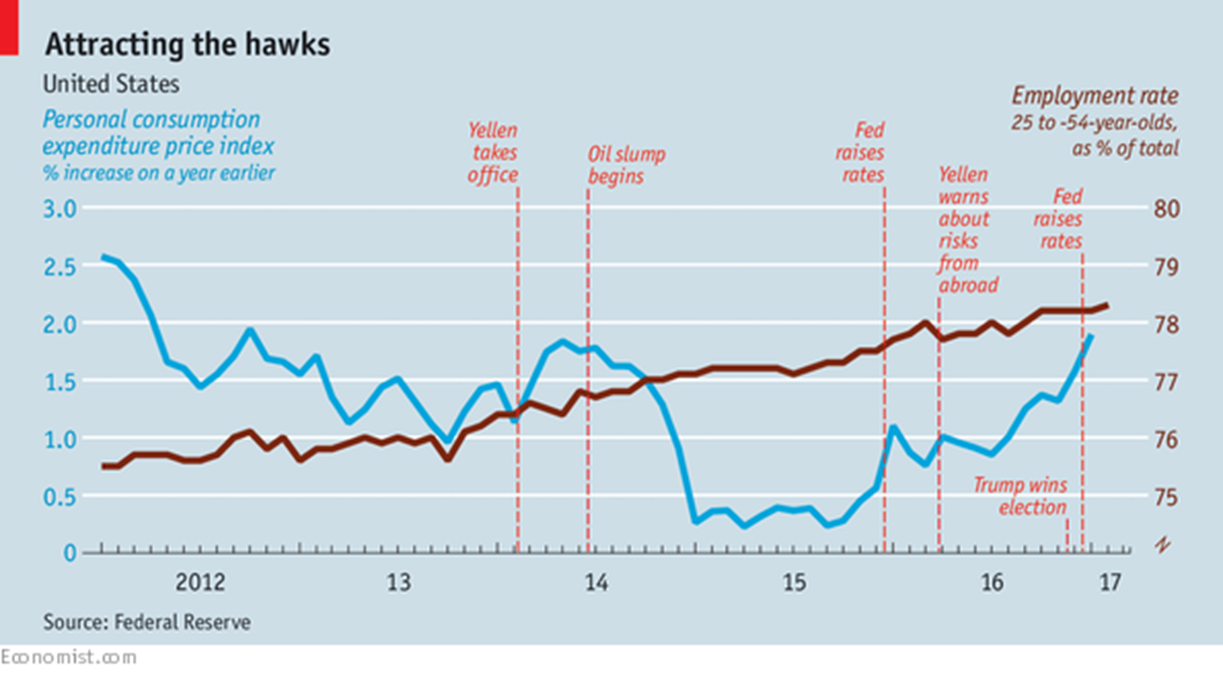

(The Economist) Third time lucky. In each of the past two years, the Federal Reserve has predicted multiple interest-rate rises, only to be thrown off-course by events. On March 15th the central bank raised its benchmark Federal Funds rate for the third time since the financial crisis, to a range of 0.75-1%. This was, if anything, ahead of its forecast, which it reaffirmed, that rates would rise three times in 2017.

“Lift-off” is at last an apt metaphor for monetary policy. But as Janet Yellen, the Fed’s chairwoman, picks up speed in terms of policy, she must navigate a cloudy political outlook. The next year will define her legacy.

Ms Yellen took office in February 2014 after dithering by the Obama administration over a choice between her and Larry Summers, a former treasury secretary. Left-wingers preferred Ms Yellen, in part because she seemed more likely to give jobs priority over stable prices. Indeed, Republicans in Congress worried that she would be too soft on inflation. The Economist called her the “first acknowledged dove” to lead the central bank.

Today Ms Yellen looks more hawkish—certainly than Mr Summers, who regularly urges the Fed to keep rates low. Headline inflation has risen to 1.9% a year; but excluding volatile food and energy prices it is a bit stuck, at around 1.7%. Yet Ms Yellen has not really changed her plumage. As expected, she has consistently given high weight to unemployment. Before her appointment, when joblessness was high, she wanted the Fed to promise to keep rates low for longer than it then planned. Now that unemployment is just 4.7%, she is keener to raise rates than those who worry about stubbornly low inflation.

In March 2015 Ms Yellen argued that, were the Fed to ignore a tight labour market, inflation would eventually overshoot its 2% target. The Fed might then need to raise rates sharply to bring it back down, risking a recession—and hence more unemployment. Better to lift rates in advance.

Unemployment, however, was already down to 5.5%. So most rate-setters had started 2015 forecasting a rapid lift-off, taking rates up by at least one percentage point over the year. But inflation remained strangely tepid (see chart). Cheap oil and a strong dollar were partly to blame. But wages also seemed stuck. Ms Yellen and her colleagues deduced that unemployment could safely fall a bit further.

In the end, they raised rates once in 2015, in December. Again, they forecast four rate rises for the next year. This time they were delayed by worries over the global economy (China wobbled early in 2016). Officials also began to see lower rates as a permanent feature of the economy.

Today, the setters think rates will eventually stabilise at 3%, down from a forecast of 4% when Ms Yellen took office.

Ms Yellen’s Fed, then, has proved very willing to change course. And this time the Fed is speeding up, rather than postponing, rate rises. Three factors are at play. First, the global economy has been reflating since the middle of 2016. Second, financial markets are booming, boosting the economy by almost as much as three interest-rate cuts, by some estimates. Third, a fiscal stimulus is looming.

According to the Fed’s model, a tax cut worth 1% of GDP would push up interest rates by nearly half a percentage point. During his campaign Donald Trump promised cuts worth nearly 3% of GDP, according to the Tax Policy Centre, a think-tank.

Doves insist that the Fed risks halting an incomplete recovery. Before the crisis of 2007-08, about 80% of 25-to 54-year-olds (the “prime age” population) had jobs. Today the proportion is 78%. The difference is about 2.5m potential workers, mostly not counted as unemployed because they are not looking for work. Were the Fed to aim for the nearly 82% prime-age employment seen in April 2000, the jobs shortfall would look twice as high.

In October Ms Yellen wondered aloud whether a “high-pressure economy”, and a resulting wage boom, might coax more people to seek work. This led to reports—soon corrected—that she would let the economy overheat after all. In fact Ms Yellen has long warned that many drivers of labour-force participation are beyond the central bank’s control. A gentle pickup in wage growth since mid-2015 seems to support her view that unemployment is the best measure of economic slack.

Rarely has unemployment been this low without inflation taking off. Once was in the late 1990s, when Alan Greenspan, a former Fed chairman, correctly predicted that rising productivity would stop a booming labour market from stoking inflation. Jeffrey Lacker, chairman of the Richmond Fed, recently offered another example. In 1965 unemployment fell to 4%, while inflation was only 1.5%.

Yet prices took off in the years that followed: by 1968, inflation had reached 4.3%.

That is what Ms Yellen wants to avoid. But the Fed has not often managed to tighten monetary policy without an ensuing recession. Should she manage it, her tenure will go down as a great success.

That is, if she has time to finish the job. Her term ends in February 2018. If Mr Trump replaces her, she could stay on as a board member. But she would probably leave. So would Stanley Fischer, the Fed’s vice-chairman, whose term expires four months later. Two of the Fed’s seven seats are already vacant, and Daniel Tarullo, the de facto vice-chairman for regulation, goes in April. So Mr Trump may be able to appoint five governors, including the chairman, within 18 months of taking office.

What then for monetary policy, and for Ms Yellen’s legacy? During his campaign, the president attacked the Fed for keeping rates low and said he would replace Ms Yellen with a Republican.

Mooted successors include Glenn Hubbard, who advised George W. Bush; Kevin Warsh, a former banker and Fed governor; and John Taylor, an academic and author of a rule, named after him, for setting interest rates.

A KETTLE OF HAWKS

All these potential successors are monetary-policy hawks. Some versions of the Taylor rule, for example, call for interest rates more than three times as high as today’s. Mr Trump, who promises revival and 3.5-4% economic growth, might not like the sound of that. If, like most populists, he wants to avoid tight money, he could appoint someone malleable to the Fed. But that would also be risky. One cause of the inflationary surge of the 1960s, notes Mr Lacker, was political pressure to keep policy loose even after ill-timed tax cuts. On one occasion, President Lyndon Johnson summoned the Fed chairman, William McChesney Martin, to berate him for raising interest rates (and to drive him around his ranch at breakneck speed).

A simpler way to keep hawkish Republicans at bay would be to reappoint Ms Yellen. With Mr Tarullo out of the frame, Mr Trump would still be able to impose his deregulatory agenda, yet keep faith with Ms Yellen to set monetary policy. Senators would struggle to come up with reasons not to reappoint a central-bank chairwoman so close to achieving her goals. Bill Clinton and Barack Obama reappointed incumbent Republican chairmen. It might be in Mr Trump’s interest to reciprocate.

March 16 – Financial Times (Robin Wigglesworth, Joe Rennison and Nicole Bullock): “When Romeo impatiently hankered after Juliet, the sage friar Lawrence dispensed some valuable advice: ‘Wisely and slow; they stumble that run fast.’ It is a dictum the Federal Reserve clearly intends to live by, despite the improving economic outlook. There have been rising murmurs in financial markets that after years of the Fed being too optimistic on the economy, inflation and interest rates, it is now behind the curve. But on Wednesday the US central bank sent a clear message to markets that it is not in a hurry to tighten monetary policy.”

Yes, markets had begun fretting a bit that a sense of urgency might be taking hold within the Federal Reserve. But the FOMC’s two-day meeting came and went, and chair Yellen conveyed business as usual. Policy would remain accommodative for “some time.” The focus remains resolutely on a gradualist approach, with Yellen stating that three hikes a year would be consistent with gradualism. And three baby-step hikes a year would place short rates at 3.0% in early 2020 (the Fed’s “dot plot” sees 3% likely in 2019). It’s not obvious 3% short rates three years from now will provide much restraint on anything. As such, the Fed is off to a rocky start in its attempt to administer rate normalization and a resulting tightening of financial conditions.

Yellen also suggested that the committee would not be bothered by inflation overshooting the Fed’s 2.0% target: “…The Fed is not inclined to overreact to the possibility that inflation could drift slightly — and in the Fed’s view temporarily — above 2% in the coming months.” There would also be no reassessment of economic prospects based on President Trump’s agenda of tax cuts, infrastructure spending and de-regulation. “We have plenty of time to see what happens.” Moreover, the Yellen Fed did not signal that it is any closer to articulating a strategy for reducing its enormous balance sheet.

Bloomberg had the most apt headlines: “Yellen Calms Fears Fed’s Policy Trigger Finger Is Getting Itchy;” “Yellen Faces New Conundrum as Conditions Defy Hike;” “The Market Is Acting Like the Fed Cut Rates.”

Ten-year Treasury yields dropped 11 bps on FOMC Wednesday to 2.49%, the “largest one-day drop since June.” Even two-year yields declined a meaningful eight bps to 1.30%. The dollar index fell 1.0%, with gold surging almost $22. The GSCI commodities index rose more than 1%. EM advanced, with emerging equities (EEM) jumping 2.6% to the high since July, 2015.

I think back to the last successful Fed tightening cycle. Well, I actually don’t recall one. Instead it’s been serial loose financial conditions and resulting recurring booms and busts. And, once again, the Fed seeks to gradually raise rates without upsetting the markets. Yellen: “I think if you compare it with any previous tightening cycle, I remember when rates were raised at every meeting, starting in mid-2004. And I think people thought that was a gradual pace, measured pace. And we’re certainly not envisioning something like that.” Heaven forbid…

In her press conference, Yellen again addressed the “neutral rate” – “The neutral level of the federal funds rate, namely the level of the federal funds rate, that we keep the economy operating on an even keel. That is a rate where we neither are pressing on the brake nor pushing down on the accelerator. That level of interest rates is quite low.”

Yellen may not believe the Fed is “pushing down on the accelerator,” yet the truck is racing down the mountain.

March 14 – Bloomberg (Claire Boston): “Companies are issuing bonds in the U.S. at the fastest pace ever… Investment-grade firms are on track to complete the busiest first quarter for debt sales since at least 1999. Firms… have pushed new issues to more than $360 billion so far in 2017, closing in on the previous record of $381 billion from 2009… That puts bond sales 14% ahead of last year’s record pace… High-yield bond offerings have also roared back after a plunge in commodity prices muted new issues last year. Junk-rated firms have sold more than $72 billion in 2017 through Monday, compared with $41.7 billion in the first quarter of 2016.”

March 16 – Bloomberg (Sid Verma and Julie Verhage): “Financial markets are telling Janet Yellen there’s more work to be done -- or else. While the Federal Reserve chair raised interest rates by 25 bps as expected Wednesday, the outlook was less hawkish than market participants foresaw, with projections for the medium-term tightening cycle largely unchanged… ‘Our financial conditions index eased by an estimated 14 bps on the day -- about 2.3 standard deviations and the equivalent of almost one full cut in the funds rate -- and is now considerably easier than in early December, despite two funds rate hikes in the meantime,’ Goldman Chief Economist Jan Hatzius and team wrote…”

The Nasdaq Composite is up almost 10%, and there’s still two weeks remaining in the first quarter. The Nasdaq 100 (NDX) has gained 11.2% q-t-d, with the Morgan Stanley High Tech Index up 13.1%. Unprecedented U.S. debt issuance could see quarterly debt sales approach a staggering $400bn. And it’s not only an American phenomenon. EEM (EM equities) enjoys a 13% q-t-d gain. Basically, stocks have posted solid early-2017 gains around the world. Corporate bond markets are booming globally. A highly speculative marketplace was delighted chair Yellen examined the current extraordinary backdrop and envisaged “even keel.”

Markets some time ago moved beyond even keel. I’ll point back to chairman Bernanke’s 2013 (“flash crash”) comment that the Fed was prepared to “push back against a tightening of financial conditions.” That was the most explicit signal yet that the Federal Reserve would backstop the financial markets to the point of guarding against even a modest “Risk Off” dynamic. Markets have hardly looked back since. Indeed, Bernanke and Yellen took “asymmetrical” (ease aggressively, “tighten” timidly) so far beyond the Maestro Greenspan. It will now be virtually impossible to convince overheated markets of a return to a more even keel policy approach.

There’s a major problem with delegating to the securities markets the critical function of governing financial conditions: loose financial conditions beget inflating asset markets. Asset inflation then begets speculation, higher asset prices, greater speculative excess and only looser financial conditions. And, to be sure, things turn especially unstable late in the speculative cycle.

Fed policies, from Greenspan to Bernanke to Yellen, provided huge competitive advantages to bullish speculative long positions. And especially since 2013 – and particularly with the policy response to last year’s market instability – the “bears” have been basically crushed into submission/oblivion. Everyone has been forced to jump aboard the bull market. This has led to a momentous supply/demand imbalance throughout the securities markets. Too much “money” has been flooding into the markets, while an atypical dynamic ensures a dearth of willing sellers. This powerful market dislocation has granted the bulls the luxury of easily pushing the market higher with little resistance from would be sellers.

Wednesday trading saw a recurring dynamic. The prospect of a hawkish FOMC meeting outcome created the risk of event-driven market instability. The hedging of risk going into this meeting created yet another opportunity to punish those on the wrong side of trades. And it’s the unwind of hedges/shorts that (for the umpteenth time) provided buying power for higher bond and equities prices. Sellers of securities – bearish traders, risk-conscious hedgers or derivative players – at this stage of the market cycle have an extraordinarily low pain threshold. The market is steeply tilted to the benefit of one side – the long side. The bulls enjoy “strong hands” – while the much-depleted ranks of weakling “bears” have about the feeblest little “weak hands” imaginable.

And the reality of the situation is that this anomalous backdrop has a profound impact on general financial conditions. Over recent decades, securities markets evolved to assume the dominant position in Credit creation, hence for system financial conditions more generally.

And, now, market dislocation creates extreme – and self-reinforcing – loose financial conditions. In the face of an alarming list of potential risks, the risk markets donned blinders and embarked on a speculative blow-off.

It’s no coincidence that markets – sovereign bonds last year and risk assets currently – have demonstrated a proclivity for “melt-up” dynamics in the face of mounting global risks. For years now, and reminiscent of the late-twenties, the fragile backdrop has ensured that central bankers cling tightly to their extraordinary monetary stimulus and market backstop measures.

Markets were beginning to feel a little anxious that the Fed might actually acknowledge market excess. Perhaps booming markets were behind the Fed’s determination to move in March rather than wait until May. And I’ll assume that the committee believed pressing for an earlier rate increase would be interpreted in the markets as a more forceful “tightening.” It’s just not going to work that away. Overheated markets at this point will dismiss timid measures. Central banker measures have for too long rewarded greed and punished fear. Greed has grown to dominate, and greed scoffs at central bank gradualism.

The problem today is that years of ultra-loose monetary conditions have ensured everyone is crowded on the same bullish side of the boat. Tipping the vessel at this point will be chaotic, and the Fed clearly doesn’t want to be the instigator. Meanwhile, timid little baby-step increases only ensure more problematic market Bubbles and general financial excess.

It’s now an all-too-familiar Bubble Dynamic. The greater the Bubble inflates, the more impervious it becomes to cautious “tightening” measures. And the longer the accommodative backdrop fuels only more precarious Bubble Dynamics, the more certain it becomes that central bankers will approach monetary tightening timidly. Yellen confirmed to the markets Wednesday that the Fed would remain timid – still focused on some theoretical “neutral rate” and seemingly oblivious to conspicuous financial market excess. The fixation remains on consumer prices that are running just a tad under its 2% target, while runaway securities market inflation is completely disregarded.

Yellen: “So at present, I see monetary policy as accommodative. Namely the current level of the federal funds rate is below that neutral rate, but not very far below the neutral rate.”

At this point, is not apparent what it would take for the Yellen Fed to change its view. It’s worth mentioning new Minneapolis Federal Reserve Bank President Neel Kashkari’s lone dissent. From Reuters: “‘The announcement of our balance sheet plan could trigger somewhat tighter monetary conditions,’ Kashkari said, resulting in the equivalent of a rate hike of unknown size. ‘After it has been published and the market response is understood, we can return to using the federal funds rate as our primary policy tool, with the balance sheet normalization under way in the background.’”

Kashkari has a point with his focus on the balance sheet. From my perspective, reducing the size of the Fed’s balance sheet would likely prove a more effective mechanism for removing accommodation than baby-step rate increases. Somehow the Fed needs to convince the markets that again boosting the Fed’s balance sheet is completely off the table. The markets believe that QE policy has simply been placed on hold, with open-ended “money” printing available the day the markets demand a liquidity backstop. The Fed should take the opportunity to ween the market off the dangerous perception that QE is available to ensure the extinction of bear markets and recessions. It’s this momentous market perception that works to ensure baby-step rate increases have no restraining impact on Bubble Dynamics.

The Fed let another opportunity slip away. One of these days the bond market may mount a protest. European periphery bonds were none too impressive. With German yields declining five bps this week, spreads widened across the board. And the dollar… It’s worth noting the yen gained 1.9% this week. And almost $5.7bn flowed out of junk bond funds.

Economista de la Universidad Católica con un master en administración en la Universidad de Harvard; periodista en economía .

¡Tú también puedes publicar! Esta es una plataforma abierta.

Cualquier persona puede crearse un blog y escribir libremente.

No necesitas ningún permiso.

Ninguna autorización.